Strategy₿, led by Michael Saylor, has pioneered a bold financial model by converting corporate capital into Bitcoin and embedding it into financial products. Through share issuances and debt instruments, the company increases its Bitcoin per share, generating what is now called “Bitcoin yield.” This strategy has attracted imitators globally and sparked debates over its sustainability, risks, and regulatory implications. Strategy₿'s approach is fundamentally anchored in sound mechanics and long-term vision. As it grows, it's not just challenging the legacy financial system; it's actively ushering in a new era of finance — one built around Bitcoin as a foundational asset, redefining how corporate treasuries, capital markets, and value preservation operate in the digital age.

“If you don't have a Bitcoin strategy, you don't have a strategy.” Michael Saylor

Taking the financial markets by storm and redefining finance as a whole, Strategy₿'s Bitcoin strategy is a new and complex concept. The intricacies of the strategy require a deep understanding of Bitcoin but also expertise of corporate finance, security analysis and other financial market components. While it is fascinating to see Bitcoin collide with traditional finance, any lack of knowledge in the aforementioned topics has led the strategy to be broadly misunderstood.

The concept has grown in popularity, leading to the emergence of numerous imitators across various jurisdictions, each adopting its own variation of the playbook. Among the most notable companies following a similar strategy are MetaPlanet in Japan, Semler Scientific in the United States, Capital₿ (formerly known as The Blockchain Group) in France, and the SmarterWeb Company in the United Kingdom, to name just a few.

In this piece, I use Strategy₿'s early version of its playbook as a case study to provide a clear, high-level overview of its Bitcoin strategy, offering straightforward explanations and addressing some of the most common misconceptions along the way. I also try to anticipate potential risks that could become threats at a later stage of Strategy₿'s journey. In order to achieve this, I answer six fundamental questions:

- Why and how did the Bitcoin strategy emerge?

- What does Strategy₿ actually do?

- How does Strategy₿ create value for its shareholders?

- How is this strategy different from other speculative attacks?

- When does this playbook end?

- What are the risks of this all?

1. Why and how did the Bitcoin strategy emerge?

In the summer of 2020, Michael Saylor, the co-founder, executive chairman of and back then Chief Executive Officer of Strategy₿, faced a critical dilemma. The company's treasury held hundreds of millions of dollars in cash, a seemingly prudent buffer during uncertain times. But with interest rates near zero and inflation fears mounting in the wake of pandemic-era monetary expansion, Michael Saylor saw that cash was quietly bleeding value. “Cash is a melting ice cube,” he famously declared, and he was not interested in watching Strategy₿'s reserves evaporate. After extensive personal research, he concluded that Bitcoin offered the best hedge against monetary debasement and presented a bold opportunity for corporate capital preservation.

In August 2020, Michael Saylor announced that the company bought $250 million worth of Bitcoin with their treasury. That decision marked the beginning of a radical corporate strategy: converting excess cash into Bitcoin and adopting it as the company's primary treasury reserve asset. It was, depending on who you ask, a straightforward strategy. Independent of Strategy₿'s software business and its future profits, a simple way of valuing the company would be to take the assets held in its balance sheet. Accordingly, Bitcoin holdings would have been valued one-to-one.

This approximation held more or less true until Strategy₿'s first $500 million bond issuance in June 2021, when the company announced they would buy Bitcoin with the proceeds of the sale. Although he did not realize it at the time, Michael Saylor had stumbled on a paradigm shift, which still holds true today: first, there is a huge demand for Bitcoin-backed fixed income products and other Bitcoin-backed securities. Secondly, Strategy₿ identified a way to acquire more Bitcoin in a manner that is accretive to Strategy₿ shareholders, increasing their Bitcoin holdings per share.

2. What does Strategy₿ actually do?

Currently many institutions cannot or do not want to hold Bitcoin directly for different reasons (such as company charters not allowing it, or Bitcoin's volatility). However, these market participants are very keen to have some exposure to Bitcoin by different means, and the appetite for Bitcoin-backed securities is tremendous. This is where Strategy₿ comes in.

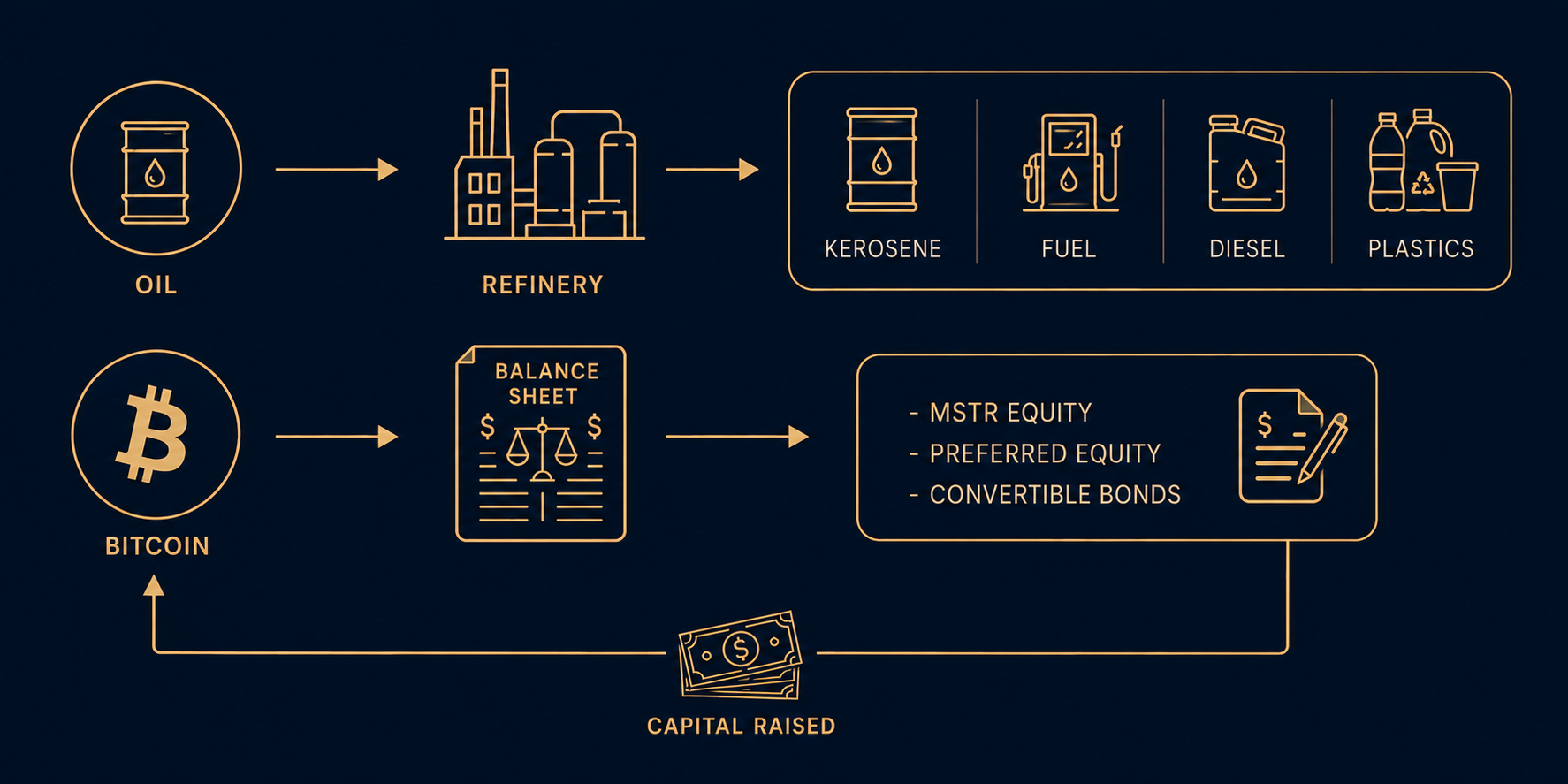

Through financial engineering and Strategy₿'s treasury operations, Michael Saylor is straddling Bitcoin to traditional finance (TradFi) by embedding Bitcoin into the various types of securities he is selling. This process can be compared to financial institutions designing and creating a structured product based on any underlying asset imaginable. Precisely this process is what Michael Saylor alludes to when he compares Strategy₿ to an oil refining company. Extending the analogy further, Figure 1 illustrates how oil represents Bitcoin, the refinery corresponds to the balance sheet, and the refined oil products (such as jet fuel, diesel, kerosene…) symbolize the various securities sold by Strategy₿.

3. How does Strategy₿ create shareholder value?

As shareholders understood the dynamics at play, they expected that Strategy₿ would hold more Bitcoin in the future for the same amount of shares by leveraging the balance sheet to acquire Bitcoin. This expectation birthed the crux of the matter: the discussion about the multiple of the Net Asset Value (or mNAV) premium on the Bitcoin held by the company. The valuation method based on the mNAV could be paralleled to the forward expectation of future cash-flows valuation, such as discounted cash-flows (or DCF), applied by analysts to value equities. In other words, the mNAV premium would be the equivalent to the expectation of the future Bitcoin holdings by the company. However, it is worth mentioning that the mNAV valuation is based on a balance sheet item, whereas traditional valuation methods are based mostly on the Profit and Loss Statement (P&L).

3.1 Defining the mNAV

Strategy₿ holds a certain amount of Bitcoin on its balance sheet. Multiplying this Bitcoin count with the Bitcoin price gets the Bitcoin Net Asset Value (or Bitcoin NAV). Basically, the Bitcoin NAV represents the market value of the Bitcoin held by Strategy₿.

The mNAV is equivalent to the multiple of the Bitcoin NAV, which is simply the Enterprise Value (or EV) divided by the Bitcoin NAV. The EV is a measure of a company's total value; it reflects the total cost to acquire a business. Thus the EV is equal to the sum of the company's current market capitalization, total debt, and total preferred stock, minus their most recently reported cash balance. The mNAV can therefore be calculated as follows:

In other words, the mNAV provides Strategy₿'s valuation, potentially with a premium or discount, on its Bitcoin held. If the mNAV is above 1, Strategy₿ trades at a premium, and if the mNAV is below 1, the company trades at a discount.

3.2 Creating shareholder value via share premium

Having a (mNAV) premium on the shares allows Michael Saylor to run his playbook. Firstly, due to Bitcoin's monetary policy (a predictable, controlled, ever-decreasing rate of inflation), expectations are that Bitcoin will increase its value in fiat terms. If Bitcoin price increases, Strategy₿'s stock price would increase too, strengthening the balance sheet as the leverage ratio to equity decreases. In turn, this allows the company to leverage up again to buy more Bitcoin, further increasing the mNAV premium on the shares. While the mNAV premium remains high, Strategy₿ can issue more shares and sell them to capture this spread, providing more Bitcoin per share and creating value for its shareholders, as explained in Example 2.

3.3 Creating shareholder value by utilizing convertible bonds

Taking a closer look at Strategy₿'s leverage, the company's initial preferred means of financing was through convertible senior notes, commonly referred to as “convertible bonds”. A convertible bond gives the holder the right to convert the bond into shares at a certain conversion price or receive back the principal amount at the maturity date. In a way, holders of these convertible bonds are given an insurance policy to the downside, should the share not perform. This additional insurance policy comes at a price, allowing Strategy₿ to set extremely low interest rates on these instruments (see Figure 2). In the meantime, Strategy₿ has evolved its playbook, shifting from convertible bonds to preferred shares. However, we will not delve into the details of this new preferred share strategy here.

| Note | Issue date | Price | Maturity | Put date | Coupon | Notional ($M) | Market val ($M) | BTC par | Ref price | Conversion price |

|---|---|---|---|---|---|---|---|---|---|---|

| Convert 2028 | 9/20/2024 | $233.52 | 9/15/2028 | 9/16/2027 | 0.625% | $1,010 | $2,359 | $60,100 | $130.85 | $183.19 |

| Convert 2029 | 11/22/2024 | $97.10 | 12/2/2029 | 6/2/2028 | 0.000% | $3,000 | $2,913 | $92,300 | $433.80 | $672.04 |

| Convert 2030 A | 3/9/2024 | $282.84 | 3/16/2030 | 9/16/2028 | 0.625% | $800 | $2,263 | $64,100 | $105.10 | $149.77 |

| Convert 2030 B | 2/22/2025 | $119.72 | 3/2/2030 | 3/2/2028 | 0.000% | $2,000 | $2,394 | $96,200 | $321.05 | $433.43 |

| Convert 2031 | 3/19/2024 | $198.01 | 3/16/2031 | 6/16/2028 | 0.875% | $604 | $1,195 | $70,500 | $166.22 | $232.72 |

| Convert 2032 | 6/18/2024 | $198.43 | 6/16/2032 | 6/16/2029 | 2.250% | $800 | $1,587 | $66,700 | $151.35 | $204.33 |

| Total / wtd avg | 4.6 yrs | 0.421% | $8,214 | $12,711 | $82,448 | $289.90 | $425.25 |

If the price of the share rallies above the conversion price, it is financially more interesting for the bond holder to convert the bond into shares. The debt turns into equity on the balance sheet and Strategy₿ does not have to pay that principal amount back. Alternatively, if the price of the share does not perform and remains under the conversion price at the maturity date, the bond holder will not convert and Strategy₿ will have to repay the principal amount. In both cases, as long as Bitcoin increases in value, the convertible bonds are accretive to shareholders. These scenarios are presented in Example 3 — scenarios 1 and 2.

In short, by leveraging up its balance sheet and selling equity, Strategy₿ is creating value for its shareholders by adding more Bitcoin per share, which Michael Saylor started referring to as “Bitcoin yield”.

4. How is this strategy different from other speculative attacks?

On October 30, 2024, during Strategy₿'s third quarter earnings call, the company announced its “21/21 Plan”. Its premise is to buy $42 billion worth of Bitcoin — $21 billion through equity and $21 billion through fixed income — over the next three years. The announcement also came with a new at-the-market (ATM) equity offering program, allowing Strategy₿ to issue and sell shares up to an aggregate offering price of $21 billion. In the meantime, Strategy₿ has completed the issuance of $21 billion in equity and, including the debt component, has achieved approximately 65% of its “21/21 Plan”. Consequently, on May 1, 2025, Strategy₿ announced it would double the scope of the plan, rebranding it as the “42/42 Plan”, with the goal of acquiring $84 billion worth of Bitcoin.

Since the first announcement, Strategy₿ has been buying Bitcoin at a staggering rate. The buying frenzy has brought many discussions. Amongst the more prominent is the concern that shareholders are being diluted when the company issues and sells more shares, which is clarified in Example 2. Another outstanding concern is that Michael Saylor is cornering the Bitcoin market, in a similar fashion as the Hunt Brothers cornered the silver market in the 80s.

In early 1980, billionaires Nelson Bunker Hunt, William Herbert Hunt and Lamar Hunt (known as the “Hunt Brothers”) started accumulating silver at a tremendous speed — up to a third of the silver not owned by governments — consequently pushing the price much higher. Silver is a commodity found in the earth's crust in abundance, and if prices are pushed up, miners will mine more as long as it remains profitable, flooding the market with fresh supply of newly mined silver. Hence, silver prices will start to decrease until there is a stabilization between supply and demand. The artificial demand and price increase created by the Hunt Brothers was short-lived.

Bitcoin, unlike silver, cannot be mined on demand. Every two weeks, the difficulty adjustment ensures that if more mining power is put into the protocol, Bitcoin mining becomes more difficult, keeping the mining schedule at a constant of a block every 10 minutes (on average). Ultimately, the supply of Bitcoin remains constant and cannot be changed. Unlike the silver miners, the Bitcoin miners cannot flood the market with new Bitcoin.

Michael Saylor, with his aggressive buying of Bitcoin, is indeed cornering the Bitcoin market — Bitcoin supply is not keeping up with his demand. However, as Bitcoin's supply cannot be increased at will, Michael Saylor should not succumb to the same fate as the Hunt Brothers.

5. When does this playbook end?

As already mentioned, if Bitcoin's price rises, so should Strategy₿ shares. As the equity increases, the balance sheet becomes healthier and allows the company to raise leverage again to buy more Bitcoin, boosting the mNAV premium on the shares. With the mNAV premium high, Strategy₿ can issue shares and sell them to capture this difference and acquire even more Bitcoin. The buying spree increases Bitcoin's price, increasing the share price again, and this becomes a feedback loop with no end in sight, which is presented in Figure 3. Strategy₿ can rinse and repeat this process many times over. Some have referred to it as the “infinite money glitch”.

The future is yet to be told; therefore, we can only speculate as to how this “glitch” ends, or at least wanes. Strategy₿ pivoted to this new strategy not too long ago and it is hard to estimate the demand for Bitcoin-backed securities. Although Strategy₿ is currently like a black hole sucking liquidity from the equity and bond markets through the constant issuance of securities at an astounding rate, the limitations will most likely come from a decrease or lack of demand for these Bitcoin-backed securities.

Assuming that fiat remains the main currency for global trade and exchange, and as Strategy₿ and other companies with the same playbook (such as Metaplanet in Japan) flood the markets with enough securities to satisfy demand, liquidity should dry up, at least for a period of time. Likely the demand will be cyclical, based on events (such as the Bitcoin halving) and other economic factors.

Interestingly, as these cycles play out, the amount of Bitcoin that Strategy₿ can buy will also decrease — mostly because of Bitcoin's scarcity, but probably also because of Bitcoin's increase in price. If this happens, all else equal and assuming Strategy₿ has not found a new way to increase its Bitcoin holdings via a new business model (such as a Bitcoin bank), the mNAV should converge back close to 1 in the long run.

6. What are the risks?

6.1 Bitcoin valuation risk

The risk that seems quite obvious is Bitcoin's price decreasing or remaining flat over the next few (three or more) years. Should this happen, Strategy₿ could run into trouble repaying the principal on the convertible bonds with maturity dates in 2027 and beyond. The outcome of such a risk is presented in Example 3 — scenario 3 above, where shareholders wind up with less Bitcoin per share. In general, any prolonged decline in Bitcoin prices undermines Strategy₿'s goals.

6.2 Antitrust regulatory risk

Strategy₿ is growing at an unfathomable rate. Eventually, it would not be inconceivable to see the company become the biggest market capitalization in the world. Regardless of whether that becomes true, a few risks could materialize, particularly if Strategy₿ keeps its current dominance with a quasi-monopoly stance on Bitcoin-backed securities — although, with the recent surge of publicly traded companies starting to copy Michael Saylor's playbook, Strategy₿ may be facing quite some competition.

Michael Saylor likes to compare Strategy₿ to Standard Oil, the company that made John D. Rockefeller the richest man in the world during the Gilded Age. Considering the fate of Standard Oil, it seems ominous to do so. Part of Standard Oil's gargantuan reach was that it bought its competitors and companies down the value chain necessary to produce refined oil products. However, it grew to such levels that it caught the eye of the government, and eventually Standard Oil was forced to be split into pieces by antitrust laws. The implied risk is whether the government could subject Strategy₿ to a similar fate.

An alternative could be the implementation of capital controls, where the government mandates that entities can hold only a limited percentage of their assets in Bitcoin. This would force Strategy₿ to liquidate a significant portion of its holdings, triggering a price crash and forcing the company to sell under unfavorable conditions.

6.3 Government asset appropriation risk

There is another risk stemming from government overreach. Similarly to Executive Order 6102, when President Franklin D. Roosevelt confiscated the gold of U.S. citizens in 1933, the U.S. government could overtake the Bitcoin on Strategy₿'s balance sheet as its own. It is important to note that this risk increases as the company accumulates more Bitcoin, potentially challenging the government's ability to counter Strategy₿'s growing dominance. This concern becomes even more relevant now that Strategy₿ is directly competing with the government in the issuance of fixed income securities. And while the risk may seem low now, it grows as Strategy₿ gains momentum and extends its lead over nation-states.

6.4 Systemic risk

It remains to be seen, but Strategy₿'s dominance (quasi-monopoly and first-mover advantage) in the market suggests that it will provide most of the Bitcoin-backed products and would get more tangled with various other big institutions in the financial markets. Reaching a certain threshold, the company may grow big enough to become a systemic risk. In this case, Strategy₿ imploding for any reason could take down the entire financial system.

Even though some of the risks mentioned may seem far-fetched, similar events have happened in the past. Mark Twain was on to something when he said: “History doesn't repeat itself, but it often rhymes.” Reflecting on the past provides a crucial perspective as we venture into uncharted territory.

Final thoughts

Strategy₿ has developed a financial strategy to generate “Bitcoin yield” by increasing Bitcoin per share through a cyclical approach. The company alternates between issuing and selling shares and leveraging its balance sheet — taking on debt mainly via preferred shares and convertible bond offerings — to acquire Bitcoin. Essentially, Strategy₿ is arbitraging the current broken financial system with its cheap money and refining it into a pristine asset: Bitcoin. Thereby Michael Saylor placed Strategy₿ on a Bitcoin Standard while simultaneously introducing Bitcoin to the capital markets — revolutionizing them in the process. However, it is worth remembering that we are still at the very early stages of this new paradigm shift, and the road ahead will surely be as volatile as Strategy₿'s price.

References

- John Roberts, Jeff. “Software firm MicroStrategy makes a massive bet on Bitcoin with a $250 million purchase.” Fortune, 11 Aug 2020. fortune.com

- MicroStrategy. “MicroStrategy Acquires Additional Bitcoins and Now Holds Over 105,000 Bitcoins in Total.” 21 Jun 2021. microstrategy.com

- MicroStrategy. “MicroStrategy Announces Third Quarter 2024 Financial Results and Announces $42 Billion Capital Plan.” 30 Oct 2024. microstrategy.com

- Strategy. “Strategy Announces First Quarter 2025 Financial Results.” 1 May 2025. strategy.com

- Walton, Jeff; Pysh, Preston. “BTC217: MicroStrategy 2025 w/ Jeff Walton.” The Investor's Podcast, 15 Jan 2025. theinvestorspodcast.com

- Kratter, Matthew. “MicroStrategy Deep Dive (Part 2).” Bitcoin University, 26 Nov 2024. youtube.com

- MicroStrategy. “MicroStrategy Announces Proposed Private Offering of $700 Million of Convertible Senior Notes.” 16 Sep 2024. microstrategy.com

- Rudolph, Barbara. “Big Bill for a Bullion Binge.” Time, 29 Aug 1988. time.com

- Nakamoto, Satoshi. “Bitcoin: A Peer-to-Peer Electronic Cash System.” 31 Oct 2008. bitcoin.org

- Bastardo, Javier. “This Japanese Company Is Playing Michael Saylor's Bitcoin Strategy.” Forbes, 29 Oct 2024. forbes.com

- Woo, Willy; Byworth, Richard. “Ep.7: Willy Woo – Money in the Next 10,000 Years: Kardashev and Beyond.” Syz the Future, 16 Dec 2024. podcast.syzcapital.com

- Chanos, Jim; Rochard, Pierre; Pysh, Preston. “BTC243: Jim Chanos vs Pierre Rochard MSTR mNAV debate.” The Investor's Podcast. theinvestorspodcast.com